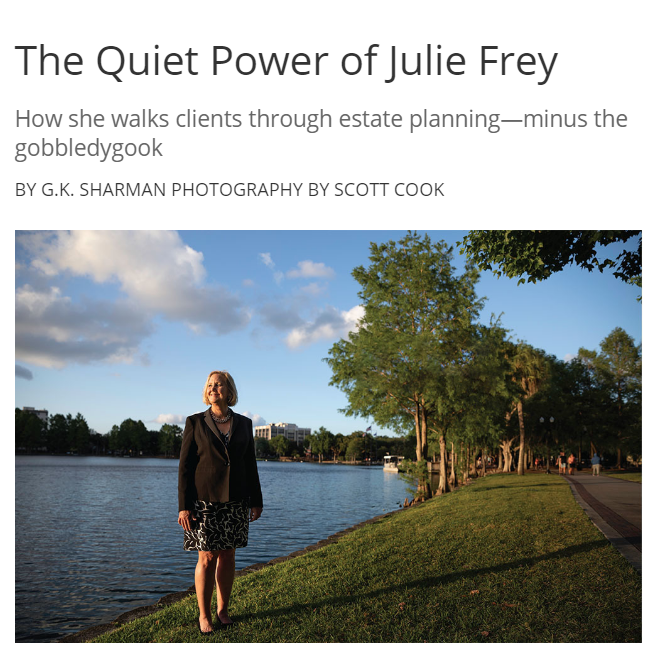

By: G.K. Sharman

Julie Frey was a shy 9-year-old when her father, prominent Orlando attorney and former Navy aviator Lou Frey Jr., ran for Congress.

By: G.K. Sharman

Julie Frey was a shy 9-year-old when her father, prominent Orlando attorney and former Navy aviator Lou Frey Jr., ran for Congress.

Lowndes attorneys obtained a favorable ruling from a probate court in Lee County, Florida, on behalf of a decedent’s estate; and thereafter, secured an affirmance of the ruling from Florida’s Second District Court of Appeal. The decedent had provided in her will for certain distributions of personal property to a beneficiary. With assistance from Lowndes probate attorney, Julie Frey, the personal representative inventoried and distributed the personal property accordingly. The beneficiary acknowledged receipt of her distribution, and filed no objections to the inventory filed by the personal representatives. Several months later, however, the beneficiary filed a petition requesting an inventory and accounting.

Lowndes trial attorney, Richard Dellinger, argued to the probate court that the beneficiary no longer had standing to request an inventory and accounting because she had already received her entire distribution of personal property. Thus, pursuant to § 731.201(23) Florida Statutes, the beneficiary was no longer an “interested party” to the estate. The probate court agreed—finding that the beneficiary had not provided sufficient evidence that she was still an “interested party”—and denied the petition. An order of discharge was entered several weeks later, but the beneficiary did not timely seek an appeal. Instead, the beneficiary filed a motion to set aside the probate court’s order of discharge on the grounds that it was not served by the probate court after entry. The motion to set aside was denied, and the beneficiary timely appealed the denial of the motion to set aside.

Lowndes appellate attorney, Jennifer Dixon, defended the appeal, obtaining a per curiam affirmance in favor of the estate. Among the arguments made to the appellate court were 1) that the motion to set aside orders did not show a colorable claim for relief because it was neither verified, nor supported by affidavits; 2) that a lack of a certificate of service on a court order is not dispositive of whether the order was, in fact, served; and 3) that orders need not be served on “non-parties,” which includes beneficiaries to an estate who have already received a complete distribution. Ultimately, the appellate court found that the probate court did not abuse its discretion in declining to vacate the order of discharge, and Attorney Frey was able to proceed in closing the estate.

As discussed earlier this summer, Treasury and the IRS identified as a burdensome regulation the Proposed Regulations under Section 2704 of the Internal Revenue Code, which regulations would severely impact discounts on gifts made to family members. (Our prior discussion can be found here.) Today, Treasury issued a report announcing that it proposes revoking the proposed regulations. This is good news for taxpayers.

By: Amanda Wilson

By: Amanda Wilson

Last summer, we discussed the IRS’s issuance of new Proposed Regulations under Section 2704 of the Internal Revenue Code, which regulations would severely impact discounts on gifts made to family members. (Our prior discussion can be found here.) Earlier this year, the Trump Administration issued an executive order instructing the Treasury Department to review all significant tax regulations issued after December 31, 2015 and identify any regulations that impose an undue burden on taxpayers. The Treasury Department and IRS have completed this review, and have identified eight burdensome regulations that should be reformed. The good news for taxpayers is that the Proposed Regulations under Section 2704 are on this list.

The next step is for the Treasury Department and IRS to recommend their proposed reform for these regulations, which could range from modification to outright repeal. We will have to wait and see what they propose, but for now, the fact that the Treasury Department and IRS targeted these Section 2704 regulations for reform is a big step in the right direction.

We will keep you updated as this process moves forward.

By: Jason Palmisano If you are not a US resident or a US citizen and are considering buying assets in the US, there are ways to avoid or minimize US estate tax on those assets. Here are some things to consider:

For tips on how to avoid or minimize US estate tax, click on the video below:

If you have any questions about US estate tax, please contact Jason Palmisano, Julie Frey or any member of the Estate Planning Group. |